It’s been one of those kind of weeks. Whistling along through earnings season...analysts trying to look busy when their bosses walk by, and vainly trying to write something intelligent about the last company conference call when the CEO said only sentences containing words like “right-culture”, “game-change”, or, “leverage” (as a verb).

Or maybe some war crime against the English language, like this:

Easy there, Tex. It’s like a consultant had his nickel batteries replaced with lithium. You can bill the client for the hours with only one or two of these words, no need to overdo it.

The FOMC comes and goes, markets go back to sleep, and then someone comes back from lunch and punches tech in the gut. Even Mohamed says BTFD.

I’m just going to keep my head down and keep doin’ what I’m doin’.

With that let's turn our attention to Asia. KRW has made a move stronger, in line with USD weakness and resilient demand in China, despite imminent fears about slowing credit growth later this year. But JPY hasn’t done much at all, owing to expectations that the BoJ is all too happy to just read the Cliff's Notes of the new #1 book in global monetary policy, “Hawkish Rhetoric for Dummies.”

That move from 1160 to 1120 is no joke...there might be an opening for a long USD/KRW position, one that is easy to get away from on a break of the recent range below 1100. IP disappointed again yesterday, and isn’t showing the positive trend for the global growth theme:

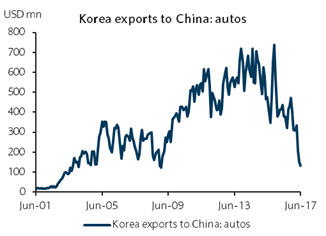

Yet some of that drag is the result of a dispute with China, which has hit auto exports hard:

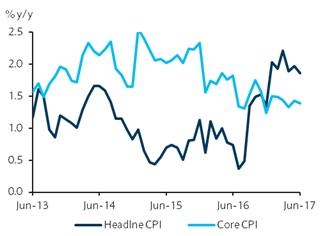

Yet overall, growth has checked up nicely from the slowdown in 2015-2016. Inflation is a bit tougher to gauge here--headline has bounced off the lows but core remains well below 2%.

This chart argues the BoK might start to hike later this year if headline CPI remains at or above 2%.

But I expect we’ll have to see core converge for that to happen, and that seems unlikely with continued strength in KRW, and little else beyond a mild fiscal stimulus program to push domestic demand.

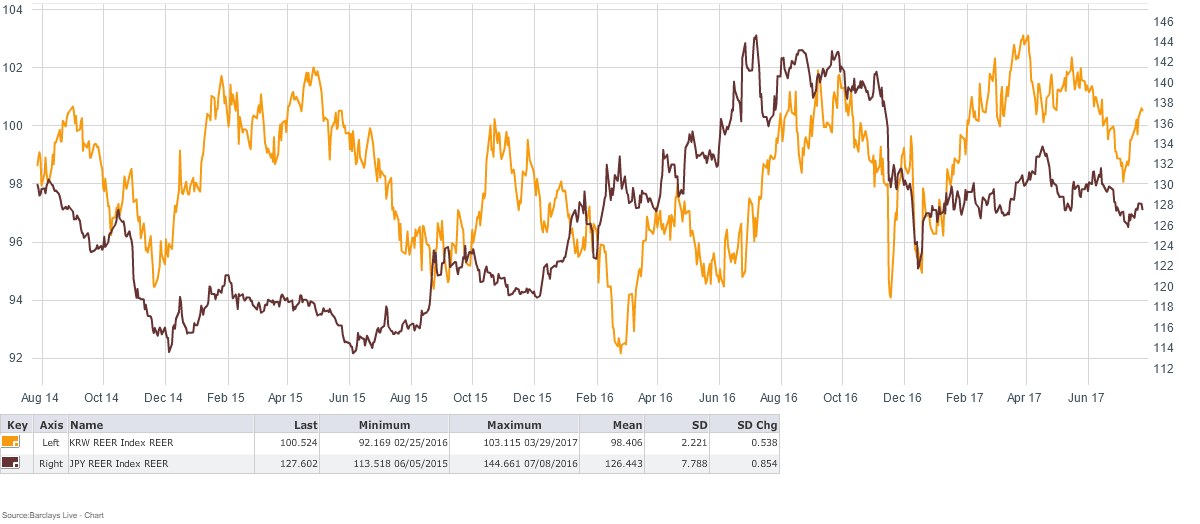

Moreover, on KRW valuation, it is getting rich vs. JPY, a key competitor in exports (and come to think of it, practically everything). REER is nearing the highs from earlier this year:

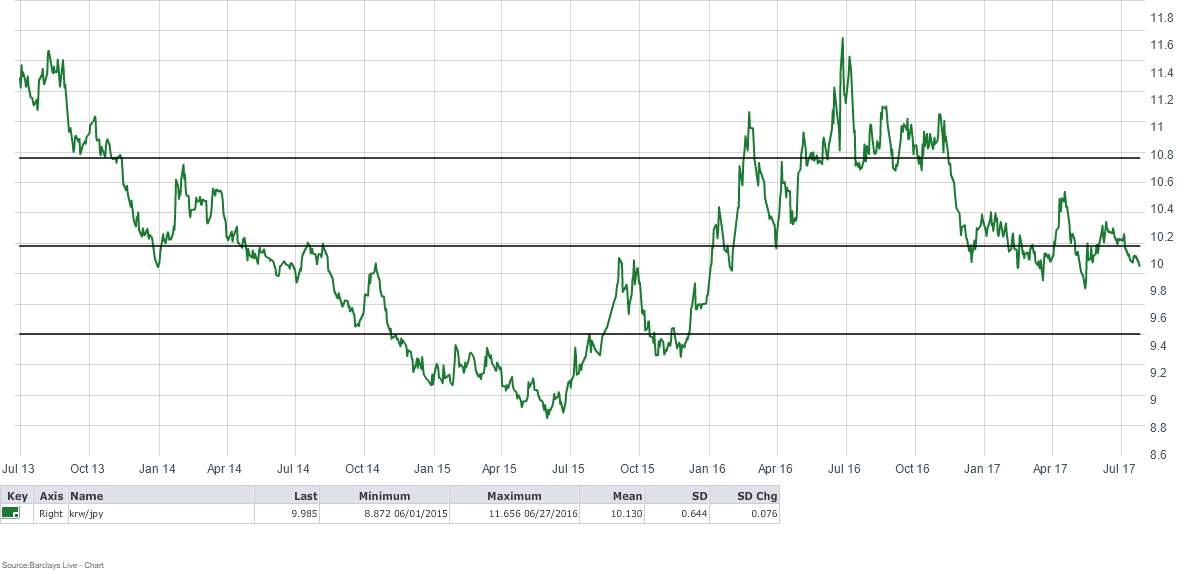

A mean reversion trade would be consistent with a bounce off of 10 in the krw/jpy cross. Tough for me to believe we are again in the JPY weakness trend that took this cross to 9 in 2015 before the BoK finally started to act.

Yet back in the US we see Trump-care a crash into the rocks, and over a cliff, back into the rocks again, before finally exploding in a fireball...sad! And Trump’s new communications director doesn’t even have the common sense to talk off the record before going on a curse-crazy rant to a New Yorker journalist.

What does that have to do with KRW? The market has gotten very complacent about (among other things) trade policy, or more broadly, Trump’s propensity for craziness, ineptitude, or some combination of all three. Should China trade, the trade deficit, or even NAFTA become a big issue again, KRW will be in the crosshairs, just like it was late last year.

That got me thinking about the long TWD idea in the comment section earlier this week--I like the theme of expressing an upswing in the tech cycle later this week via Asia FX, but at these levels I would like some protection against the unexpected:

Sure, Korea’s monstrous current account surplus still needs to get recycled somehow...but history shows KRW is prone to get whacked much harder than TWD if rates go higher, USD strengthens, FTQ returns, or China rolls over….it carries flat, and as I mentioned, is setting up nicely to take the other side.

Adding a short KRW position to long positions in TWD or elsewhere in the region looks like a good beta-weighted overlay...the correlations are high but that could be a positive, foreshadowing a spell of underperformance given the technicals and the rich valuation of KRW on a REER basis and vs. JPY. A USD call/KRW put would lay off enough squirrelly risk to enable much larger core positioning.

7 comments

Click here for commentsAnother great post, Shawn. Thank you. Think you're right to question outright USDTWD exposure. Though I'm short, the correlation between tech stock performance and TWD, in particular, has me nervous.

ReplyOrgasm every time I check EURCHF/vol.

Decided to trade against my own euphoria and took off EURCHF cash position, replacing with some vega-neutral RKO calls. Momentum seems to have slowed today and wanted to protect PnL too. We'll see whether it was the right thing to do.

ReplyDarth Macro (on Twitter) mentioned the setup in USDJPY this weekend, pointing to extreme long positioning in the COT data as we approach a possible debt ceiling showdown. USDJPY looks a bit low on a regression, but JPM pitched an interesting 109-107 put spread with 105 RKI on bottom strike put. Not much extra premium versus vanilla for a lot of extra gearing. Looking at the USDJPY versus US 10Y, <105 corresponds to the pre-election/dis-inflation regime. My thought is that while we may get a scare, we probably don't go back to that regime, so I like the 105 level for that RKI.

Thinking about CLP these days. Shawn mentioned as a good China hedge given the low carry, however, regressed on copper and rates, it looks cheap. Also, elections are coming up later this year which may see business-friendly Pinera replace Bachelet. Interesting setup. Re copper, you have the 19th Congress and still strong tier-3 real estate markets in China, and just last week, a new ban on scrap imports that require dis-assembly, which is like 80% of China's scrap imports (and scrap imports are 15-20% of China's supply).

Anyone has explanation for EUR strength? 1.183 against USD already? I am little bit perplexed...

ReplyHey Johno...i'm with you on taking profits, or protecting them anyway, in eur/chf. that is a big, big, move on not a lot of news.

ReplyRe: CLP...first PEN, now CLP? We should talk...

The copper/CLP correlation is a slippery one. I think you have to think back to the 2004-2012 period (see BdCh multilateral currency measure link below) to see what copper prices can do to the currency there--the wild increase in prices spurred a massive spike in FDI and domestic demand, and drove huge c/a surpluses and the currency to insane levels. That's not the case today. Chile also has a history of very whippy inflation...right now we're in the downcycle--and without the stimulus from high copper prices (FDI and revenues), I don't think there will be an ignition for a quick acceleration of growth and inflation--in fact, if anything BdCh is leaning towards cutting more, not the other way around. If high copper prices spur growth and inflation to a point where the central bank sought to increase real rates, I'd feel differently.

Re: Pinera, I think there is risk here too--I guess Pinera II will be an improvement on Bachelet II, but he's not going to have a mandate for radical business friendly change. If the last four years have taught us anything it is that the electorate is fed up with the establishment. I don't think popular discontent is strong enough to elect a guy like Guillier, but you can't rule it out either.

http://si3.bcentral.cl/Siete/secure/cuadros/arboles.aspx

Thank you, Shawn. Appreciate the feedback very much!

ReplyIt’s like a consultant had his nickel batteries replaced with lithium

Replyดูหนังฟรี2022

dramaslist2u.com

despite imminent fears about slowing credit growth later this year

Replyดูหนังฟรีออนไลน์

movie123-days.com